EB-5 Bridge Financing Under Threat: Proposed DHS Rule

DHS's proposed July 2026 EB-5 rule could reshape bridge financing. Learn what leading immigration attorneys say, key changes, and what investors should know.

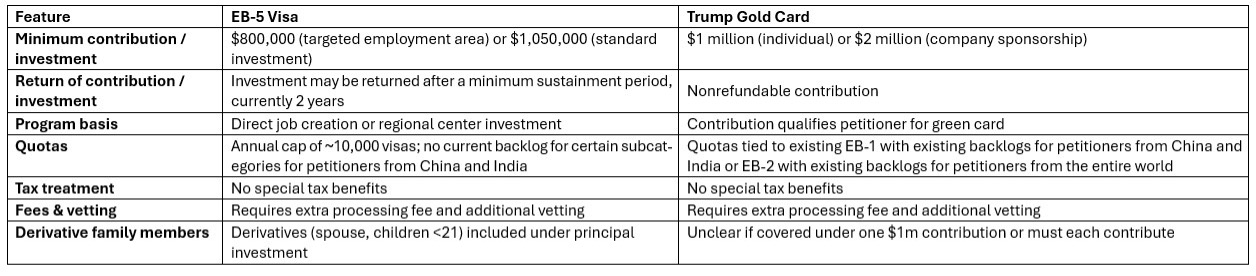

The new Trump Gold Card program was implemented by White House Executive Order (the ”EO”) on Friday, September 19, and further publicized on the Trump Card website after several months of preparation.

The Gold program offers a pathway to U.S. residency distinct from the EB-5 visa. Instead of requiring investment in a job-creating project which applicants can receive back within a few years, individuals can qualify by making a $1 million contribution (or $2 million if sponsored by a company), which they never get back.

Unlike EB-5, which is tied to new job creation and regional center investments, the Gold Card is tied to existing EB-1 or EB-2 categories, which also have quota limits like EB-5, and have existing backlogs. The Gold Card does not provide favorable tax treatment, and applicants must pay an additional processing fee and undergo extra vetting. It is also unclear whether derivative family members are included under a single $1 million contribution or if each must contribute separately.

The bottom line: people considering immigrating to the U.S. based on the EB-5 immigrant investor visa should apply now.

Trump's executive order requires the government to implement the Gold Card within 90 days of publication, so by December 18, 2025. While the EO includes an obscure mention that the government will “Consider expanding the Gold Card program to visa applicants under EB-5", it remains unclear how this could happen by executive order rather than by passage of legislation by Congress. Current law provides that any EB-5 petitioner submitting their petition before September 30, 2026 will be adjudicated under existing rules.

The most conservative approach for those considering EB-5 would be to apply before the December 18, 2025 deadline for Gold Card implementation.

The Trump Card website also refers to a Platinum card as “coming soon”, which would require a $5 million contribution, and offer recipients exemption from US income taxes on non-U.S. income and allow recipients to spend up to 270 days in the US. Note that the Platinum Card has not yet been implemented.

If you are considering the EB-5 immigration by investment visa, Contact Peachtree Group to learn more about the process.